Tax Cuts and Jobs Act (TCJA)

The Tax Cuts and Jobs Act (TCJA) was signed into law on December 22, 2017. This legislation contains substantial changes to the U.S. income tax system. TCJA affects all sectors of our economy, but the following information will only discuss the parts of TCJA that directly impact agriculture.

-

Most provisions of TCJA were scheduled to take effect for tax years beginning after December 31, 2017.

-

Most provisions of TCJA will expire after 2025 but some provisions are permanent.

Tax rates and brackets

Under TCJA, federal individual tax rates change (beginning in 2018) but are scheduled to expire after 2025.

-

New federal tax brackets include: 10, 12, 22, 24, 32, 35 and 37 percent.

-

These brackets replace the old brackets of: 10, 15, 25, 28, 33, 35 and 39.6 percent.

In the past, the thresholds for each of the brackets were indexed for inflation.

-

The new brackets under TCJA are indexed for inflation under a “chained consumer price index (CPI).”

-

This will result in smaller annual adjustments to the brackets.

Capital gains

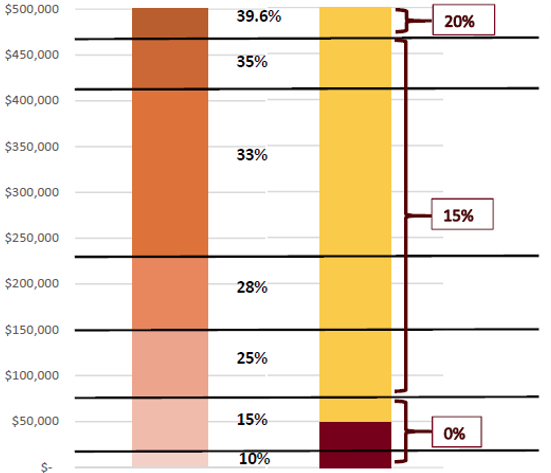

Under the old rules, capital gains rates included: 0, 15, 20, 25 and 28 percent.

-

Capital gains rate was 0 percent if all taxable income (including the capital gain) remained below the top of the 15 percent bracket.

-

Capital gain that landed between the top of the 15 percent bracket and the top of the 35 percent bracket was taxed at 15 percent.

-

Capital gain that landed in the 39.6 percent bracket was taxed at 20 percent.

Figure 1 displays how capital gains rates interacted with income tax rates.

In Figure 1, the left bar represents the old tax rates for 2017. The right bar represents where the breaks for the various capital gains rates were in 2017. Under TCAJ, the breakpoints for the 15 and 20 percent capital gains/qualified dividends rates are set as statutory dollar amounts and adjusted for inflation.

See Figure 2 for the capital gains rates for married filing joint (MFJ), head of household (HOH), single and married filing separate (MFS).

Figure 2: 2018 Capital gains rates

| Capital gains rates | Joint filers (MFJ) and surviving spouses | Head of household (HOH) | Single | Married filing separate (MFS) | Estates and trusts | |

|---|---|---|---|---|---|---|

| 0% | < | $75,900 | $50,800 | $37,950 | $37,950 | $2,550 |

| 15% | < | $470,700 | $444,550 | $418,400 | $235,350 | $12,500 |

| 20% | ≥ | $470,700 | $444,550 | $418,400 | $235,350 | $12,500 |

Standard deduction and personal exemptions

Effective for 2018, TCAJ substantially increased the standard deduction and eliminated all personal exemptions. See Figure 3 for standard deduction amounts.

Figure 3: 2018 standard deduction

| Filing status | 2017 | 2018 |

|---|---|---|

| Single or MFS | $6,500 | $12,000 |

| MFJ or QW | $13,000 | $24,000 |

| HOH | $9,550 | $18,000 |

| Age 65 and/or blind MFJ, QW or MFS Single or HOH | $1,250 $1,550 |

$1,300 $1,600 |

- MFS - Married filing separately

- MFJ - Married individuals filing joint returns

- QW - Qualifying widow(er)

- HOH - Heads of household

Kiddie tax

Kiddie tax applies to “unearned” income of children that are:

-

Less than age 19.

-

College students less than age 24.

Unearned income is typically investment income. Earned income is W-2 wage income and farm income reported on Schedule F.

-

The final threshold amount for 2018 has not been posted at this time.

-

The 2017 threshold was $2,100.For kids over age 17, the kiddie tax applies only to children whose earned income does not exceed one-half of the amount of their support.

Beginning in calendar year 2018, the tax rate for dependents that meet the kiddie tax test will be taxed not at the parents’ tax rate, but rather at the estate and trust rates.

Child tax credit

Effective for tax year 2018, the child tax credit is increased to $2,000 per qualifying child. The credit is available for a qualifying child under the age of 17. Income phase-outs exist for the child tax credit.

The Tax Cuts and Jobs Act also created a credit for qualifying dependents.

-

The new $500 credit is for a qualifying dependent age 17 or older.

-

This child or relative must meet the dependency requirements.

-

If the dependent is a child, the dependent needs to be under age 19 at the end of the year, or a full-time college student who is age 24 or less at the end of the tax year.

-

A disabled child of any age qualifies for the credit (must meet dependency requirements).

Charitable contributions

Taxpayers who are able to itemize can include charitable contributions on their tax return.

-

TCJA increased the limitation from 50 percent of Adjusted Gross Income (AGI) to 60 percent of AGI.

Gift of commodity

Farmers are encouraged to consider gifts of commodities as charitable contributions.

-

When you gift a commodity, the farmer does not have to report the income.

-

The farmer is still able to deduct the production expenses associated with growing the commodity.

Gift of grain

A gift of grain needs to be given the year after the crop was produced.

-

Under Revenue Ruling 55-531, a farmer is not allowed to deduct the production costs of grain used for a gift in the year of production.

-

If grain is gifted in the same year of production, Schedule F costs should be reduced in proportion to the amount of the gift of grain.

Rules for charitable contributions

Rules for charitable contributions differ from the rules for gifts.

-

Charitable contributions made in the same tax year as produced or grown do not require a reduction of schedule F expenses [Reg. 1.170A-1(c)(4)].

-

The farmer does not get an itemized charitable deduction for the charitable contribution of the commodity.

-

But, expenses connected to the production of the grain will be deducted on Schedule F.

-

The gifted grain is not included in income thus reducing regular and SE tax, according to Harris in Agricultural Tax Issues.

Affordable Care Act

TCAJ does not change anything in 2018 related to the Affordable Care Act (also known as Obamacare).

-

In 2019, the penalty for failing to maintain minimum essential coverage for individuals is repealed.

-

Net Investment Income Tax (NIIT) remains unchanged.

Corporate rates

Tax rates for C-corporations are reduced to 21 percent beginning with tax years starting after January 1, 2018. This provision of TCAJ is permanent.

Alternative minimum tax (AMT)

For tax years beginning after December 31, 2017, C-Corporations are no longer subject to AMT. C-Corporations with an AMT credit may offset regular tax liability (moving forward). Phase-outs will apply.

TCAJ retains AMT for individuals. New legislation temporarily increases (through 2025) the AMT exemption. This has made it more difficult for individuals to qualify for AMT.

Domestic production activities deduction (DPAD)

Domestic production activities deduction (DPAD) is repealed for tax years beginning after 12/31/18.

- Elements of DPAD still remain with respect to the new qualified business income calculation (QBI).

- Many cooperatives run fiscal years that differ from the calendar year. It is possible that producers could receive a pass-through DPAD from the cooperative because the current tax year (or currently reportable) tax year began before 12/31/18.

- Any cooperative DPAD pass-through will be reported on Federal Form 1099-PATR.

Like-kind exchanges (LKE)

TCAJ modified the like-kind exchange rules so that only real property qualifies.

-

Real property includes land and any property attached to the land.

-

This law change effectively eliminates non-recognition of gain on a machinery trade.

Under the old LKE rules, a taxpayer (in this case, a farmer) trades a piece of equipment on a newer piece of equipment. As long as the farmer did not receive any money in the transaction, the gain is postponed and any cash paid plus the old basis in the equipment becomes the new equipment basis.

-

Under the new rules, the traded piece of machinery traded will be treated as an outright sale.

-

For most cases, this will result in depreciation recapture (ordinary income not subject to self-employment tax).

Machinery trade - example 1

-

Farmer Jones trades an old combine for a new one. The dealer allows farmer Jones $200,000 on the trade and farmer Jones pays an additional $250,000 to boot to complete the purchase.

-

Under the old method, farmer Jones does not recognize any gain on the trade. Assuming that the old combine has zero basis, farmer Jones’ basis in the new combine is the $250,000 paid to boot (Figure 4).

Figure 4: Machinery trade (old method)

| Action | FMV | Cash paid |

|---|---|---|

| Trade combines | ||

| Old combines (traded unit) | $200,000 | |

| New combine | $450,000 | $250,000 |

Machinery trade (new method under TCAJ) - example 2

-

Same circumstances as the example above. Assuming no basis in the combine to be traded.

-

Farmer Jones will recognize $200,000 of depreciation recapture (reported on Form 4797, Part III).

-

Farmer Jones will pay the full price ($450,000) for the new combine. (Figure 5)

-

Strategy: Farmer Jones has a large Section 179 allowance that could be used and/or bonus depreciation on the purchase of the new combine. Using accelerated depreciation could offset the depreciation recapture from the sale of the traded combine.

-

The State of Minnesota will recognize the like-kind-exchange of the machinery trade described above. If the like-kind-exchange qualified under the old pre-TCJA rules, the taxpayer is required to recognize the LKE on the State of Minnesota return.

Figure 5: Machinery trade (new method under TCAJ)

| Action | FMV | Cash paid |

|---|---|---|

| Trade combines | ||

| Old combine (traded unit) | $200,000 | |

| New combine | $450,000 | $450,000 |

Machinery trade under TCAJ - example 3

-

Guy and Barb Wire are trading a tractor purchased in 2013 for a new tractor in 2018. The implement dealer allows Guy and Barb a $100,000 allowance on the traded tractor and the Wires pay a cash price of $225,000 for the new tractor.

-

The relinquished tractor had an original purchase cost of $170,000 and has a remaining tax basis of $41,658. Guy and Barb did not take any section 179 or bonus depreciation on the relinquished asset at the time of purchase.

-

The relinquished tractor is sold on IRS Form 4797 (part III). Guy and Barb’s gain on the sale of the tractor is $58,342 ($100,000 allowance minus remaining basis of $41,658). This gain is depreciation recapture (code Section 1245 gain), which is taxed as ordinary income and is not subject to self-employment tax. See Figure 6 for a copy of Guy and Barb's Federal Form 4797.

-

The gain from the sale of the traded tractor is qualified business income (QBI). More information about QBI is discussed in another section.

Net operating losses (NOLs)

Two-year carryback and special carryback provisions are repealed except for losses incurred in the business of farming (ag no longer has a five-year carryback).

NOL carryovers are allowed indefinitely (changed from 20 year limit under old rules).

-

TCJA limits the NOL deduction (absorption) to 80 percent of the taxable income in the carryback/carryforward year.

-

In other words, an NOL cannot zero out all taxable income in any given year. The new rules set forth by TCAJ only affect NOLs incurred in 2018 moving forward.

-

This provision still needs clarification by Congress or the Internal Revenue Service.

Depreciation

-

New farm machinery for tax years beginning after 12/31/17 will be classified as 5-year property instead of 7-year property.

-

Used farm machinery will still be classified as 7-year property.

Farm assets in the 3 to 10 year class life are eligible for 200 percent DB method.

-

The previously approved method was 150 percent DB method.

-

200 percent DB method provides a higher percentage of depreciation in the first years of use.

Farm assets in the 15 and 20-year class life still use 150 percent DB method.

Example: comparison of 150 and 200 percent DB method

Farmer Jones purchased a combine in 2017 for $430,000. Farmer Jones did not take section 179 or bonus depreciation on the new combine.

-

Farmer Jones; depreciation for 2017 will be $46,071 ($430,000/7 x .5 x 150%).If Farmer Jones had purchased the same combine in 2018 the depreciation deduction would be $86,000 ($430,000/5 x .5 x 200%). This is an increase of $39,929.

Section 179

TCAJ increased the section 179 limit to $1 million. Investment phase-out begins at $2.5 million. The SUV limitation remains at $25,000.

-

Previously defined property eligible for section 179 is still eligible under TCAJ.

-

Generally, this property includes property with a depreciable life of three through 15 years.

-

TCAJ expanded the definition of qualifying section 179 property to include:

-

Roofs.

-

Heating, ventilation and air conditioning property.

-

Fire protection and alarm systems.

-

Security systems.

-

Property used predominantly to furnish lodging, such as furniture and appliances.

-

Computers and peripheral equipment are removed from the definition of listed property.

-

Section 179 and Minnesota

The State of Minnesota does not recognize the new qualifying property added to the section 179 list from the Tax Cuts and Jobs Act.

-

In other words, Minnesota will not recognize section 179 on roofs, heating, ventilation and air conditioning property.

-

Any section 179 taking on the federal return for the newly added assets from TCJA will need to be added back on the Minnesota return.

After establishing the qualifying property for the State of Minnesota return for section 179:

-

The state will allow a 100 percent deduction for the first $25,000.

-

For all amounts above $25,000, an 80 percent add-back is required.

In other words, the taxpayer will get a 20 percent deduction for the excess amounts in the current year and a 20 percent deduction in the four subsequent years.

Bonus depreciation

TCAJ expanded the use of bonus depreciation to 100 percent for assets purchased between September 28, 2017 and December 31, 2022.

-

TCAJ changed the requirements for bonus depreciation to include new or used property (formerly first use requirement is repealed).

-

For a taxpayer’s first tax year ending after 9/27/2017 (2017 calendar year taxpayer), a taxpayer may elect to apply a 50 percent allowance instead of 100 percent allowance.

Bonus depreciation and Minnesota

The State of Minnesota is also de-coupled from the Federal rules for bonus depreciation (Additional First-Year Depreciation).

-

Similar to Section 179, Minnesota does not recognize the most recent changes for bonus (i.e., used property and the 100 bonus rate).

-

Prior to the TCJA, the federal bonus percentage was scheduled to be at 40 percent for 2018. This is where the State of Minnesota begins the calculation.

State of Minnesota calculation

-

First, all bonus depreciation taken on used assets on the federal return will not qualify for Minnesota and needs to be added back (i.e., used equipment).

-

Then the taxpayer takes assets with bonus depreciation elections from the federal return.

-

The taxpayer reduces the 100 percent allowance to 40 percent.

-

The 60 percent excess is added back to the basis of the asset for Minnesota depreciation purposes.

-

From the 40 percent bonus depreciation, an 80 percent add-back is performed for the entire 40 percent amount.

Minnesota bonus add back - example 5

Farmer Jones purchased a new utility tractor for $60,000. Farmer Jones elected to take 100 percent bonus on the asset for Federal tax purposes.

-

For Minnesota, farmer Jones must reduce the $60,000 of bonus from the federal return to 40 percent of the purchase cost (($24,000) $60,000 x .4 = $24,000). The excess $36,000 gets added to the basis of farmer Jones’ utility tractor on the Minnesota depreciation schedule.

-

The 40 percent bonus depreciation amount for 2018 is $24,000. Eighty percent of the $24,000 will need to be added back as income reducing the 2018 bonus expense for the new utility tractor to $4,800 ($24,000 x .2 = $4,800).

Bonus depreciation percentage will begin to phase-down beginning in 2023 and go to zero in 2027. See Figure 7 for phase-down schedule.

Bonus depreciation percentages

| Placed in service year | Qualified property in general/specified plants | Longer production period property and certain aircraft |

|---|---|---|

| Jan. 1, 2017-Sept. 27, 2017 | 50% | 50% |

| Sept. 28, 2017-Dec. 31, 2022 | 100% | 100% |

| 2023 | 80% | 100% |

| 2024 | 60% | 80% |

| 2025 | 40% | 60% |

| 2026 | 20% | 40% |

| 2027 | None | 20% |

| 2028 and thereafter | None | None |

Most farm assets will be included in the second column (qualified property in general/specified plants). Longer production period property will include 15 and 20-year property (drainage tile and single-purpose ag. structures).

Meals for employees – fringe

Meals provided to employees for the convenience of the employer have been 100 percent deductible in the past.

-

TCAJ modifies the meals for employee rules so that expenses for employer-operated eating facilities are only 50 percent deductible through 2025.

-

In 2026, the aforementioned meal expenses become nondeductible.

Federal estate and gift tax

TCAJ increased the federal exclusion amount to $11,180,000 for 2018.

Each individual has an annual gift exclusion of:

-

$14,000 – couples together total $28,000 – 2017.

-

$15,000 – couples together total $30,000 – 2018.

Each individual has a life-time gift exclusion equal to the federal estate tax exclusion:

-

$5,490,000 for 2017.

-

$11,180,000 for 2018.

Section 199

Section 199 refers to the domestic production activities deduction (DPAD).

-

TCAJ repeals DPAD for tax years beginning after 12/31/17.

-

Although TCAJ repeals DPAD, elements of the DPAD calculation remain with the addition of Section 199A (AKA the grain glitch).

Section 199A

Passage of the original legislation for TCJA contained what has come to be known as the “grain glitch”. Farmers that sold to a cooperative opposed to selling to a private business were given a huge incentive.

-

Sales to co-op: 20 percent pass-through deduction based upon gross sales.

-

Sales to non co-op: 20 percent pass-through deduction based upon the net.

Passage of Section 199A caused a great deal of anxiety and confusion in that producers recognized the significant financial benefit of selling to a cooperative entity versus a non-cooperative entity.

Please note that the passage of Section 199A was intended to address an incentive for all non-corporate business entities. C-corporations are not eligible for a section 199A deduction (qualified business income or QBI).

Consolidated appropriations act (CAA)

The Consolidated Appropriations Act modified TCAJ with respect to sales to cooperatives. The 20 percent deduction is based on qualified business income (QBI).

QBI is defined as:

-

Qualified items for income, gain, deduction and loss with respect to a qualified trade or business of the TP.

-

Items are qualified only to the extent that they are connected with the conduct of a trade or business in the U.S.

Items that are excluded from QBI:

-

Net capital gain or net capital loss.

-

Dividends, income equivalent to a dividend, or payments in lieu of dividends.

-

Interest income.

-

The excess of gain over loss from commodities transactions other than:

-

Those entered into in the normal course of the trade or business, or

-

With respect to stock in trade or property held primarily for sale to customers in the ordinary course of the trade or business, property used in the trade or business, or supplies regularly used or consumed in the trade or business.

-

-

The excess of foreign currency gains over foreign currency losses.

-

Net income from notional principal contracts other than clearly identified hedging transactions that are treated as ordinary.

-

Any amount received from an annuity that is not received in connection with the trade or business.

QBI for lease income

Lease income may be eligible for qualified business income deduction (QBI).

-

Currently, IRS guidance indicates that in order for lease income to be treated as QBI, the lease arrangement must meet the qualification of a trade or business under IRS Code Section 162.

-

Trade or business is not specifically defined in the Internal Revenue Code but rather defers to case law for guidance.

-

Under case law, trade or business may be established by involvement with continuity and regularity and where the primary purpose is income/profit.

Please note that QBI for leases is a huge gray area. The author can make a compelling argument that land held for cash rent is classified as “held for investment”, rather than a trade or business.

One part of this argument that is settled is self-rentals.

-

A self-rental is an arrangement where an entity such as a C-corporation is paying land rent to the owner of the land.

-

The owner of the land also is the owner of the C-corporation.

-

The key to this provision is “common control”.

-

Rental payments made under a self-rental situation does qualify as QBI [Treasury Regulation 107892-18].

It is recommended for cash land leases to not take the QBI deduction until some additional guidance is issued from either the IRS or the courts.

-

Crop share leases and Conservation Reserve Program contracts come much closer to meeting the test of trade or business than a cash lease.

-

Please consult with your tax professional on this issue.

20 percent pass-through deduction as specified by CAA

-

For taxable years beginning after 12/31/2017 and before 01/01/2026.

-

An individual taxpayer may deduct 20 percent of qualified business income from a partnership, S corporation, or sole proprietorship, as well as 20 percent of the aggregate, qualified Real Estate Investment Trust (REIT) dividends, and qualified publicly traded partnership income.

For cooperatives, the new Section 199A deduction is essentially the same thing as the old domestic production activities deduction (DPAD). For cooperatives, the section 199A deduction is the lesser of:

-

9 percent of QPAI (qualified production activities income).

-

9 percent of the taxable income without the QBI deduction.

-

50 percent of the W-2 wages.

The above calculation will be made at the cooperative level.

-

The cooperative may elect to use the credit or pass the credit on to the patron.

-

If the credit is passed through to the patron, that business activity will be reported on Form 1099-PATR.

-

If the farmer receives a pass-through QBI credit from the cooperative, the aforementioned credit is not subject to the taxable income restrictions found under the regular QBI calculation.

-

If the farmer receives a pass-through credit from the cooperative, the farmer may report the credit against income on his or her Federal Form 1040.

Basic QBI calculation

A taxpayer’s QBI is the lesser of:

-

20 percent of the qualified business income (QBI), or

-

20 percent of (taxable income less capital gains).

Basic QBI calculation - example 6

The following information is from Farmer Pat’s tax return:

-

Taxable income of $81,000.

-

Schedule F net of $100,000.

-

No capital gains.

Farmer Pat’s QBI deduction is the lesser of:

-

20 percent of taxable income ($81,000 x .2 = $ 16,200)

-

20 percent of QBI ($100,000 x .2 = $20,000)

Pat’s eligible QBI deduction is $16,200.

Basic calculation with capital gain - example 7

This example has the same circumstances as the previous example, except Pat also had a $7,000 net capital gain.

Pat’s QBI deduction is the lesser of:

-

20 percent of (taxable income less capital gains) ((20 percent of ($81,000 minus $7,000) = $14,800).

-

20 percent of QBI ($100,000 x .2 = $20,000)

Pat’s eligible QBI deduction is $14,800.

Transition rule regarding DPAD and QBI calculations for producers with sales to cooperatives

The Consolidated Appropriations Act includes a transition rule for farmers who receive a cooperative payment in 2018 that is attributable to QPAI (qualified production activities income) for which the old DPAD (domestic production activities deduction) deduction was applicable.

-

This will include any QPAI attributable to a cooperative tax year beginning before 2018. See Section 101(c)(2).

With the original DPAD gone in 2018, taxpayers were left to wonder how to report such DPAD allocations.

-

The law clarifies that such farmers will still be able to take the old DPAD deduction in 2018, as long as it is attributable to QPAI which was allowed to the cooperative for a tax year beginning before 2018.

-

No 199A deduction will be allowed for such payments [Appropriations Act Sec. 101(c)(2) Division T].

Impact to farmers

Most cooperatives operate under a fiscal year.

-

The transition rule will affect farmers that did business with a cooperative with a tax year that started before 12/31/17 (which will be true in most cases).

-

Cooperatives with a tax year beginning before 12/31/17 will still be able to calculate and potentially distribute a DPAD to the cooperative patrons.

-

If the farmer receives a DPAD passed through from the cooperative, the farmer will be able to use the DPAD on his or her 2018 income tax return.

The transitional rule excludes from the 199A QBI calculation any sales from the farmer that falls within the co-op’s fiscal year.

-

It does not matter whether the cooperative passed the DPAD through to the patrons or retained the DPAD at the cooperative level.

-

All farm sales that occurred during the cooperative’s fiscal year will NOT be eligible income for the QBI deduction on the farmer’s 2018 individual return.

Transition rule regarding DPAD and QBI calculations for 2018 - example 8

Farmer Jones sells corn and soybeans to ABC Cooperative.

-

ABC Cooperative has a fiscal year that began August 1, 2017, and ended July 31, 2018. Fiscal years will vary by the cooperative.

-

Since ABC Cooperative’s fiscal year started before 12/31/17, ABC will be able to calculate and potentially distribute a DPAD credit to its patrons.

-

A pass-through DPAD credit will be reported on Form 1099-PATR and the aforementioned DPAD credit will be reported on Farmer Jones’ 2018 individual income tax return.

-

Farmer Jones must exclude farm sales made to ABC Cooperative that occurred between January 1 and July 31 (the end of the co-op's fiscal year) from the QBI calculation.

-

The only co-op sales that Farmer Jones will be able to use for the 2018 QBI calculation will be sales that occurred after July 31.

-

Sales that occurred during the fiscal year of the cooperative that was eligible for DPAD at the cooperative level do not qualify as QBI income.

-

It does not matter whether ABC retained or distributed the DPAD credit.

With the passage of the Consolidated Appropriations Act (CAA) the QBI deduction for the farmer changes. The formula for QBI deduction if sales to a cooperative are involved is:

-

20 percent of overall QBI (both co-op and non co-op)

-

Reduced by the lesser of:

-

9 percent of the QBI from the trade or business allocable to the cooperative payments, or

-

50 percent of the wages allocable to the cooperative payments

-

NOTE: When taxable income is above certain thresholds (MFJ $415,000/All other filers $207,500), wages paid and qualifying assets come into play for the QBI calculation.

QBI calculation with 100 percent sales to cooperative (no wages) - example 9

Farmer Pat has the following information on the tax return:

-

All commodity (grain) sold through cooperative.

-

$230,000 per unit retains.

-

$20,000 patronage dividend.

-

$200,000 expenses – no wages paid.

-

$50,000 QBI ($230k + $20k - $200k).

Calculation

-

20 percent x 50k = $10,000

-

Reduced by the lesser of:

-

9 percent x $50k (all sales were to cooperative) = $4,500

-

50 percent x $0 (zero wages paid by farm) = $0

-

Pat’s QBI deduction is $10,000 ($10,000 minus zero).

QBI calculation with 100 percent sales to cooperative (with wages) - example 10

Farmer Pat has the following information on the tax return:

-

Circumstances for this example are the same as the previous example except Pat paid $25,000 in wages.

Calculation

-

20 percent x 50k = $10,000

-

Reduced by the lesser of:

-

9 percent x $50k (all sales were to cooperative) = $4,500

-

50 percent x $25,000 = $12,500

-

Pat’s QBI deduction is $5,500 ($10,000 minus $4,500).

NOTE: The cooperative calculation is still subject to the 20 percent of (taxable income less capital gains) limitations.

NOTE: If the cooperative elects to pass-through the credit calculated at the cooperative level, that pass-through amount will get added to the calculated figure in this example.

QBI calculation with 60 percent sales to cooperative (no wages) - example 11

Farmer Pat has the following information on the tax return:

-

60 percent of commodities (grain) sold through cooperative.

-

$230,000 per unit retains.

-

$20,000 patronage dividend.

-

$200,000 expenses – no wages paid.

-

$50,000 QBI ($230k + $20k - $200k).

-

60 percent of overall QBI was allocable to the co-op ($50,000 x .6 = 30,000).

Calculation

-

20 percent x 50k = $10,000

-

Reduced by the lesser of:

-

9 percent x $30k (all sales were to cooperative) = $2,700

-

50 percent x $0 (zero wages paid by farm) = $0

-

Pat’s QBI deduction is $10,000 ($10,000 minus zero).

NOTE: If the cooperative elects to pass-through the credit calculated at the cooperative level, that pass-through amount will get added to the calculated figure in this example.

QBI calculation with 60 percent sales to cooperative (with wages) - example 12

Farmer Pat has the following information on the tax return:

-

60 percent of commodities (grain) sold through cooperative.

-

$140,000 per unit retains.

-

$10,000 patronage dividend.

-

$100,000 of non-cooperative sales.

-

$200,000 expenses – $25,000 wages paid.

-

$50,000 QBI ($140k + $10k + $100k - $200k).

-

60 percent of overall QBI is allocable to the co-op ($50,000 x .6 = $30,000).

-

60 percent of wages is allocable to the co-op ($25,000 x .6 = $15,000).

Calculation

-

20 percent x 50k = $10,000

-

Reduced by the lesser of:

-

9 percent x $30k (portion allocable to the sales to the co-op) = $2,700

-

50 percent x $15k (wages paid by farm) = $7,500

-

Pat’s QBI deduction is $7,300 ($10,000 minus $2,700).

Tax planning

-

Any crop insurance proceeds you receive need to be included as income on your tax return.

-

You generally include that income in the year received.

-

Crop insurance includes the crop disaster payments received from the federal government as the result of destruction or damage to crops, or the inability to plant crops because of drought, flood, or any other natural disaster.

You can postpone reporting crop insurance proceeds as income until the year following the year the damage occurred, if you meet all the following conditions:

-

You use the cash method of accounting.

-

You receive the crop insurance proceeds in the same year the crops are damaged.

-

You can show that under normal business practice you would have included income from the damaged crops in any tax year following the year the damage occurred.

Currently, deferral of crop insurance or disaster payments is considered an all or none proposition. This topic can be complicated. Please check with your tax professional.

If you use the cash method of accounting to report your income and expenses, your deduction for prepaid farm expenses in the year you pay for them is limited to 50 percent of the other deductible farm expenses for the year (all Schedule F deductions minus prepaid farm expenses). This limit does not apply if you meet all the exceptions described below:

-

Many cash-basis tax filers utilize prepaid expenses at year-end to balance expenses with income.

-

This practice also allows farm producers to guarantee delivery and lock-in prices on crop inputs for the following year.

Prepayments must meet the following conditions:

-

Must be for an actual purchase and not a deposit.

-

The prepayment has a business purpose and is not merely for tax avoidance.

-

The prepayment does not result in a material distortion of income, according to The Farmers Tax Guide.

There are a couple of exceptions. The limit on the deduction for prepaid farm expenses does not apply if you are a farmer and either of the following applies:

-

Your prepaid farm expense is more than 50 percent of your other deductible farm expenses because of a change in the business operations caused by unusual circumstances.

-

Your total prepaid farm expense for the preceding three tax years is less than 50 percent of your total other deductible farm expenses for those three years.

The maximum prepaid amount is calculated each year based upon the final figures on the Schedule F.

-

Fall-applied fertilizer and lime does get treated differently.

-

If fertilizer and lime are purchased late in 2016 and applied before January 1, 2017, the fertilizer and lime expense is not considered a pre-payment for tax purposes and thus is not subject to the 50 percent rule, according to The Farmers Tax Guide.

Case farm example to show the interaction of business income and QBI

We will go back to the example earlier in the paper where Guy and Barb Wire traded tractors.

Example: trading tractors

-

Guy and Barb Wire are trading a tractor purchased in 2013 for a new tractor in 2018. The implement dealer allows Guy and Barb a $100,000 allowance on the traded tractor and the Wires pay a net cash price of $150,000 for the new tractor.

-

The relinquished tractor had an original purchase cost of $170,000 and has a remaining tax basis of $41,658. Guy and Barb did not take any section 179 or bonus depreciation on the relinquished asset at the time of purchase.

-

The relinquished tractor is sold on IRS Form 4797 (part III). Guy and Barb’s gain on the sale of the tractor is $58,342 ($100,000 allowance minus remaining basis of $ 41,658. This gain is depreciation recapture (code section 1245 gain), which is taxed as ordinary income and is not subject to self-employment tax.

-

Tax planning: Guy and Barb could take section 179 or bonus depreciation on the new tractor in order to offset some or all of the $58,342 gain from the traded tractor. Guy and Barb need to consider the following items:

-

Taking accelerated depreciation (section 179 and bonus) will lower or take the Schedule F negative for 2018. This results in no SE tax paid and can have a negative impact with respect to disability insurance and retirement benefit.

-

By taking accelerated depreciation, Guy and Barb are using depreciation that would normally reduce ordinary and self-employment tax. By taking the Schedule F negative, they are buying down cheap money with expensive money.

-

Taking accelerated depreciation will also lower the qualified business income (QBI) deduction. Please note that in this example, the net schedule F and also the depreciation recapture is QBI income.

-

If Guy and Barb create negative QBI in 2018, the negative QBI carries forward (similar to a Net Operative Loss) and must be offset by positive QBI in a subsequent year before Guy and Barb will qualify for a QBI deduction.

-

Case 1

-

This example has the Wires with a schedule F showing a net of $35,000 before any accelerated depreciation.

-

One child (under age 17).

-

Wage income of $30,000 with federal withholding of $3,600.

Case 2

-

This example is the same as example 1, except the Wires took accelerated depreciation on the new tractor to the degree that the Schedule F shows a negative $40,000.

-

This lowers the tax due.

-

This practice also significantly lowers the qualified business income deduction.

See Figure 8 to get an overview of how the two cases differ.

Note: This information piece is offered as educational information only and is not intended to be tax, legal or financial advice. For questions specific to your farm business or individual situation, consult with your tax preparer.

- RIA Checkpoint (online service) checkpoint.riag.com

- National Association of Tax Professionals www.natp.com

- Thomson Reuters Complete Analysis of the Tax Cuts and Jobs Act 2017. Hoboken, NJ

- Land Grant University Tax Education Foundation. www.taxworkbook.com

- TheTaxBook.com

- The Farmers Tax Guide. Publication 225. www.irs.gov

- www.irs.gov

- CCH Tax Briefing. Tax Cuts and Jobs Act.

- Joint Committee on Tax. www.jct.gov

-

Harris, P. E., Agricultural Tax Issues, Fall 2012. p. 187

-

The Tax Book. TCJA Supplement. Summer Edition 2018. Tax Materials Inc. www.thetaxbook.com

-

2015 Publication 225. The Farmers Tax Guide. pp. 19-20 www.irs.gov

Reviewed in 2019